Since Park Piedmont Advisors’ founding in 2003, we’ve been writing a series of newsletters and sharing them with our clients and friends. These original writings cover a wide array of financial topics, as well as our thoughts on the bubbles, booms, busts, and bailouts we’ve guided our clients through.

We are delighted to share these articles with you – to illustrate how we believe in thinking for ourselves, not following the herd. For example: read what we were thinking in the depths of the financial crisis in late 2008 and early 2009.

Please contact us if you’d like to read or learn more.

We’re honored to share that Park Piedmont has been named a ThinkAdvisor Luminaries Award 2024 Finalist for Thought Leadership and Education.

What is a ThinkAdvisor Luminaries Award?

From ThinkAdvisor:

ThinkAdvisor’s Luminaries Awards redefine excellence in financial services, shining a spotlight on outstanding contributions from both organizations and individuals.

“The 2024 Luminaries Awards continue to push the boundaries of what excellence means in the financial services industry,” said Janet Levaux, editor-in-chief of ThinkAdvisor.

“This year’s finalists have not only demonstrated exceptional leadership and innovation but have also shown a deep commitment to making a positive impact on their communities and the industry at large. Their contributions are a testament to the dynamic and evolving nature of our business, and we are proud to highlight their achievements as examples for others to follow.”

To view the list of finalists, visit the ThinkAdvisor website. ThinkAdvisor will announce the award winners in December.

Thought Leadership & Education

Innovating on behalf of our clients’ education and growth has always been central to the work at Park Piedmont. Since our founding over two decades ago, we have shared monthly – and, more recently, biweekly – original commentary on money and markets, provided pro bono financial literacy education to young adults, published a book on investing, and co-created a mini-curriculum for families around money, values, and relationships.

Most recently, we launched Money, Meet Meaning, a unique podcast exploring the surprising, practical relevance of the world’s spiritual traditions on our life with money. The podcast is co-produced with Interfaith America, the nation’s premier interfaith organization. In each episode, guests of varying spiritual backgrounds share insights into how their tradition paves a path for navigating our complex financial lives.

We are glad to receive this recognition. Ours is a crowded industry, and so many other, far larger firms leverage seemingly endless marketing budgets to flood prospective clients’ attention. We prefer to use education as a way to both reach prospective clients and connect with current clients.

More than that: we have considered client education an essential aspect of our fiduciary role. We spend a great deal of time and energy to create content that is interesting, accessible – and above all, helpful for our clients.

So while we are glad to spend a moment in the spotlight, rest assured, our focus remains where it’s always been: on you.

Much has been reported about the Federal Reserve’s reducing interest rates by 50 basis points, lowering the federal funds rate to a range of 4.75% to 5%. The move represents a pivot from the past two years of rate hikes, which were designed to combat inflation, and signals the Federal Reserve’s conclusion that inflation — down to 2.5% from a peak of 9.1% in mid-2022 — is now under control.

Does the Fed’s move warrant any substantive shift in your overall investing strategy? For our Park Piedmont clients, we would answer: probably not.

Unquestionably, the Fed’s rate reduction will have some impact on varying asset classes.

For savers, the 5-percent-plus yields on money market funds, available over the past couple years, will shift downward. Nevertheless, there may well be a continuing role for investing in cash equivalent money market funds in light of each of our client’s particular circumstances – even though the yields will turn lower.

For bond investors, falling interest rates mean that available yields will decline. Going forward, as new bonds are issued at lower rates, the extent of interest income to be earned will decline somewhat for savers. But the news isn’t all bad, since falling interest rates mean the price of existing bond prices will rise. (Recall that by contrast, when interest rates are rising, bond prices decline.)

For riskier assets like stocks, there is an oft-repeated consensus that stocks tend to perform well after interest rate reductions. That’s because when the Fed reduces rates, one of its objectives is to make borrowing less pricey for consumers and businesses alike, boosting economic productivity. But a recent study by Morningstar cautions investors, noting that “the last four major rate-cutting cycles show why it’s challenging to draw sweeping conclusions. Market performance can vary dramatically in the year after a new [Fed-initiated] easing cycle starts.”

At Park Piedmont, our approach to investing relies on developing an appropriate asset allocation based on each of our clients’ particular circumstances, with a focus on your goals, risk tolerance, and the time horizon for use of your financial assets. Shifts in fiscal policy and accompanying changes in investor sentiment are inevitable for investors, and typically do not call for any adjustment in overall asset allocations.

What might warrant possible rebalancing?

Perhaps your need for the use of your money has changed – either you need money sooner or later than originally anticipated when establishing your asset allocation. Or perhaps you recognize that your emotional tolerance for risk and volatility has changed. Or perhaps the movement of market prices has altered your initial asset allocation significantly enough to justify restoring your asset allocation to its original position.

In any of these cases, your Park Piedmont advisors are here as helpful resources. If you have questions, don’t hesitate to reach out.

Trust is at the core of the relationship between client and advisor. That’s why trustworthiness is one of Park Piedmont’s core firm values, guiding the way we approach our work.

Firm Value: Trustworthiness

There are many ways we strive to make sure this value of trust shows up in our day-to-day work: acting as a fiduciary, always putting your (and all of our clients’) best interest before our own; being straightforward, honest, and responsive; and doing what we say we’ll do.

Cybersecurity is another important area where we’re building trust with you. Park Piedmont, in collaboration with Schwab and our other technology partners, has implemented various protections to ensure the security of our clients’ sensitive personal and financial information.

Beware Spear Phishing

Our Client Service team recently attended a Schwab conference, and one of the driving themes throughout the conference was the increased sophistication of scammers, along with the importance of fraud prevention to protect our clients.

In particular, the Schwab cybersecurity experts informed the conference that “spear phishing” attempts are on the rise. These targeted attacks are highly personalized and often appear to come from a trusted source, such as a colleague or even your advisor. The aim is to trick you into sharing sensitive information or clicking on malicious links. We have heard from clients about similar schemes.

To protect yourself from these attacks, please be vigilant for any unsolicited communications requesting personal information or prompting urgent action. If you receive anything suspicious, please feel free to notify your advisor. Our team will work with our outside information technology partner to confirm if the request is legitimate.

Use Schwab’s e-Authorization Tools

An additional layer of trust around your personal information: Schwab’s eAuthorization tools make this sort of fraud much more difficult. Even if the fraudster has access to your email address, they’re unlikely to also have access to your Schwab Alliance credentials or mobile device. Since multifactor authentication is required through these channels, eAuthorization is the best, safest, fastest way to conduct transactions for our clients, while at the same time protecting against fraud.

Expect Verbal Verification

We have also implemented a new policy requiring verbal verification for all one-time Move Money transaction requests from clients. You can still send in these requests via email, but before we process anything, your Park Piedmont advisor or a member of our Client Service team will reach out via phone call to verbally confirm that the request is legitimate.

(We want to be clear that this new policy only applies to one-time requests. If you have a recurring monthly distribution from your Schwab account, we will continue to process those transfers as normal.)

These changes mean you might be hearing from us more frequently – we look forward to it!

The Importance of Trust

In closing, we know well that trust is an ongoing process. Please be in touch with your valuable input and any feedback – we are eager to continue to earn your trust every day.

Park Piedmont’s mission is to help our clients gain clarity and peace of mind in their life with money. In doing so, we promise fiduciary guidance that’s principled, personal, and practical.

Personal and practical are fairly straightforward — but what do we mean by “principled”?

Park Piedmont has ten firm values. Each one informs the way we work with our clients and the way we work with one another. Some values are demonstrated in our investment philosophy or approach to ongoing education. Others inform how we communicate. Still others characterize the posture we strive for when showing up to work each day.

To keep our firm values top of mind, we take turns during weekly team meetings recognizing our colleagues and sharing specific examples of how our values are reflected in our work.

This weekly practice keeps the importance of our mission in front of us – and reminds us that the way we do our work matters.

In our Life with Money newsletter, we’ll highlight and describe one firm value at a time to demonstrate the ways they inform our principled approach to our work and our relationships with our clients.

The point of the discussion was to present some of the personality traits that can become obstacles to successful long-term investing:

“Changing how people think about the money they save for retirement is a central tenet of a movement based on behavioral finance, the approach to economics that aims to understand how average people, not rational economists, make financial decisions. After all, it’s the way people behave around money that tends to derail their plans, not a lack of knowledge about what they need to do if they want to retire comfortably.”

The article, written by Paul Sullivan, discusses ways behavioral finance helps people save more for retirement and also helps people “limit their investment choices, so they would need to opt out of a broadly diversified portfolio, which is the portfolio most likely to produce the best returns over time.”

The primary article in The New York Times “Your Money” section, “Why We Think We’re Better Investors Than We Are,” was written by Gary Belsky. The article starts by explaining why Behavioral Finance focuses so many of its studies on the investment markets – because they “provide unusually robust data sets for analyzing ‘judgment under uncertainty,’ … how people make choices when resources are at stake and the outcome is unknown.” The article then comments on the “sunk cost fallacy,” which causes investors to focus on their original cost, not wanting to sell at a loss, representing “a nonconscious desire to justify their earlier decision.” This idea feeds into the “key tenet of ‘loss aversion,’ which tells us that humans typically respond to the loss of resources – be it time, emotion, material goods or their proxy, i.e., money – more strongly than they react to a similar gain.

The article continues:

“Despite the spectacular growth of index funds – passive investment vehicles that track market averages and minimize transaction costs – millions of amateur investors continue to actively buy and sell securities regularly. This despite overwhelming evidence that even professional investors are no more likely to beat the markets than a monkey throwing darts at security listings. Money managers, at least, are paid to make investment bets. But why do amateurs believe they can outperform the professionals – or even identify those pros who will outperform?”

(Performance of mutual funds cannot be predicted with any greater degree of accuracy than individual stocks or bonds).

Many biases and cognitive errors contribute to this costly behavior, but a few deserve mention.

Overconfidence: “The tendency to overrate our abilities, knowledge and skill, at whatever level we place them … There is a disconnect between actual and perceived financial sophistication, evidence of how widespread the overconfidence bias is.”

Optimism bias: “Helps explain why many investors believe they can outperform the market.”

Hindsight bias: “The tendency to rewrite our own history to make ourselves look good … People consistently misremember their forecasts, in ways that make them look smarter.”

Attribution bias: “When remembering our failures, we remember them in a way that neutralizes their ability to inhibit our present-day decisions. When events unfold that confirm our thoughts or deeds, we attribute the happy outcome to our skills, knowledge, or intuition. But when life proves our actions or beliefs to have been wrong, we blame outside causes over which we have no control.”

Confirmation bias: “Giving too much weight to information that supports existing beliefs and discount that which does not … Once one entertains the idea that this seems like a good investment, the processing of relevant information narrows considerably – and in a direction that leads to over confidence.”

The final pertinent article in the “Your Money” section was written by University of Chicago Professor John List. The general point made by Professor List is that, because of loss aversion, people underinvest in the stock market. They look at their investments too frequently, and when they see declines, they sell their stock positions in order to avoid further declines. This behavior occurs even though people are aware of the long-term outperformance of stocks:

“Market research shows that when your horizon is not today, not next week, but way in the future, the most profitable strategy is to invest more heavily in riskier assets – stocks – than people are prone to do. So why don’t people invest more in stocks? … Because people are loss averse … keenly more aware of losses than comparable gains … Those who evaluate their investments frequently, see lower returns on their risky assets like stocks … So what can be done? Not paying too much attention to your portfolio is a good first step.”

More specifically, List’s advice – which he says he follows – is to look at one’s portfolio no more than once every three to six months.

The Thaler book presents all the behavioral finance ideas and their chronological development. We have presented a few highlights that relate specifically to investing.

On investing for the long term:

“The equity premium is defined as the difference in returns between equities (stocks) and some risk-free assets such as short-term government bonds … With a 6% edge in returns, over long periods of time such as 20 or 30 years, the chance of stocks doing worse than bonds is small … (But) the more often people look at their portfolios, the less willing they are to take on risk, because if you look more often, you will see more losses … Defined as myopic loss aversion, those who saw their results more often were more cautious … So the equity premium, the required rate of return on stocks, is so high because investors look at their portfolios too often.”

But in an important footnote, Thaler comments that “this is not to say stocks always go up … they quite recently fell 50%, which is why the policy of decreasing the percentage of stocks in your portfolio as you get older makes sense.”

In a chapter devoted primarily to John Maynard Keynes, he quotes Keynes as follows:

“Day to day fluctuations in the profits of existing investments, which are obviously of an ephemeral and non-significant character, tend to have an altogether excessive, and even an absurd, influence on the market.” – John Maynard Keynes

Thaler writes:

“Keynes was also skeptical that professional money managers would serve the role of smart money, but rather they were more likely to ride a wave of irrational exuberance than to fight it … as it is risky to be a contrarian … and that professional money managers were playing an intricate guessing game, similar to their judging a beauty contest, where the winning judge is the person who picks the faces of those who most of the other judges picked as the prettiest, rather than the faces that he (the judge) thinks are the prettiest.”

In another chapter, Thaler writes:

“When prices diverge strongly from historical levels (our note: that is, long-term average valuation measures such as price/earnings ratios), in either direction, there is some predictive value in these signals. And the further prices diverge from historic levels, the more seriously the signals should be taken. Investors should be wary of putting money into markets that are showing signs of being overheated, but also should not expect to be able to get rich by successfully timing the market. It is much easier to detect that we may be in a bubble than it is to say when it will pop, and investors who attempt to make money by timing market turns are rarely successful.”

Finally, in our extensive experience with individual investors, we would add one more item to the list of behaviors that cause problems: the financial media’s emphasis on day-to-day activity, which turns many people into short-term investors, with the negative outcomes observed by the behavioral finance group. When the short-term results of financial markets are turned into a sports event, or a casino, as they are often reported on by the media, it becomes difficult for even the most disciplined of investors to ignore the “noise” and focus on their long-term objectives. At Park Piedmont, we view overcoming this challenge as a major priority.

In case you missed it, we’re re-publishing the note we wrote originally on August 5, 2024, when the S&P 500 stock index declined by 3%. Stocks have been up and down since, with the S&P gaining 2.3% on August 8. This is yet another example of why it’s impossible to make short-term predictions about market movements, and why it’s therefore best not to react to large declines, since you might miss an eventual recovery.

• • •

The US and other world stock markets have declined significantly over the last few weeks. We have no way of predicting what will happen, of course, but we think it’s helpful to put these declines in context.

We hope this provides some comfort going forward. As always, we’re available to discuss any of these topics at your convenience.

Broadly diversified stock indexes and funds have fallen since their recent peaks on July 16. The S&P 500 index is down 8.5% in this period, while Vanguard’s total US stock fund has declined 9.1% and Vanguard’s total world stock fund (including US, developed and developing country international stocks) is down 7.7%.For 2024 year-to-date, however, all three of these indicators are still up between 6% (world stock) and 9% (S&P 500). Despite recent less-good news on employment and consumer spending in the US, which appear to be a significant factor in the recent sell-off, the US and world economies have seen declining inflation and positive economic growth for the year.

While stock prices have declined, bond prices have risen significantly in 2024. Bond prices rise when interest rates fall, and the benchmark 10-year US Treasury has gone down from 4% at the start of the year to 3.78% currently. The declines are more dramatic compared with the 4.9% level in October of 2023 and 4.7% as recently as April of this year.There are many factors involved in falling interest rates, including reduced inflation and expectations of upcoming rate cuts by the US Federal Reserve. In any case, the rising bond prices have served to cushion diversified portfolios against the stock price declines, as also happened during 2000-02 (“dot com bust”) and 2007-09 (“Great Recession”).

Stock price declines happen regularly. The most recent market correction (generally defined as a decline of 10% from a previous high) occurred from August through October of 2023. No one likely remembers that now, since it happened in the middle of a year when stock markets around the world rose more than 20%. Stocks fell more than 30% in the early months of the pandemic in 2020, but quickly recovered to gain around 20% by the end of that year. Recoveries from the larger declines in 2000-02 and 2007-09 took longer, but generally occurred within a couple of years.The key point is that you only benefited from the recoveries if you stayed invested in the markets. Anyone who sold during these admittedly difficult, often scary periods had to decide when to buy back into the markets, and potentially missed the recoveries completely.

This brief history highlights a few important investing concepts:

Trust your asset allocation. All of our Park Piedmont clients have customized plans for investing in a diversified portfolio of riskier (generally stocks and high-yield income investments) and less risky (generally bonds and cash) assets. These are designed to meet your specific long-term needs and goals, and account for your time horizon and risk tolerance (see discussion in Jeff Sommers’ article, “Why You Should Be Taking a Hard Look at Your Investments Right Now,” in The New York Times on August 2). That means the allocations are supposed to help you to live through the occasional downturns, with the understanding that you’ll participate in recoveries and do well when the markets rise. If that’s not the case, please let us know and we can revisit your asset allocation.

Re-balance as appropriate. The Sommers article mentioned above highlights the importance of regular re-balancing, or returning to your target allocation when one asset class has drifted significantly from its target. The stock market gains since 2022 might have pushed your stock allocation above your targets, for example, while the recent declines might have brought the stock allocation back into line. We review re-balancing opportunities regularly on your behalf.

Re-invest over time. If re-balancing does make sense for you, we recommend making any changes over time instead of all at once. This is referred to as “dollar cost averaging” and represents an attempt to mitigate the risk of making a large change all at once.

Again, your Park Piedmont advisors are here to discuss any of these topics and answer your questions, as they arise.

Estate planning is a vital piece of any financial plan. No matter how well a person has saved and invested their money over time, inaction or procrastination when it comes to wills, trusts, and beneficiary designations can have disastrous consequences. Without valid, up-to-date documents in place, one’s assets may be distributed in suboptimal ways – either because the intended beneficiaries don’t receive them and/or because they are subjected to unnecessary fees.

What Is the Probate Process?

When a person dies, their estate is “opened,” and the probate process begins. This process involves the disbursement of the deceased’s assets to creditors and beneficiaries under a judge’s supervision. If the deceased has a valid will, their wishes will typically be honored by the judge, unless the repayment of debts or taxes depletes what is left for heirs. A will may also be contested by anyone who believes they are entitled to more than what the will provides them, which can complicate and lengthen the process.

Probate law varies from state to state, but in general, assets that are subject to probate include anything left to an heir via a will or when no valid will exists. Additionally, any assets where the ownership is classified as sole ownership, tenancy in common (TIC), or community property (CP) will be allocated to heirs via probate.

The Downsides of Probate

While probate can fulfill a deceased person’s wishes for how their estate is dispersed, there are a few downsides – it can be very expensive (due to legal fees) and time consuming (if there are many competing claims from creditors and heirs, or many assets to sort through, etc.).

Additionally, the court proceedings are public record, so there is no privacy for the deceased and heirs in how property is doled out. So, it is often in one’s best interest to keep as much property out of probate as possible.

How to Avoid Probate

Common methods of avoiding probate include passing property “via contract” to named beneficiaries, as well as titling property in certain ways. Examples of contracts that bypass probate include life insurance, annuities, retirement accounts such as IRAs and 401ks, trust accounts, and transfer on death (TOD) accounts. A TOD account is essentially an individual investment account that has a beneficiary. If there is no living beneficiary named for these types of assets, they will be brought back into the probate process.

Another way to avoid probate is to change the titling of property to be owned jointly. With this form of ownership, when one property owner passes away, the other joint owner(s) automatically receive the deceased’s portion.

All these methods of bypassing probate allow the deceased person’s property to pass directly to their beneficiaries without the need for a court order. It is important to note that with these same methods, the beneficiary designations supersede the deceased’s will. If a will provides instruction for the disbursement of specific assets that are held in accounts that bypass probate, the will will be ignored when it comes to that property. Instead, it will pass directly to the named beneficiaries outside of the probate process. For example, if a person’s will says that they intend to leave their 401k to their son, but the named beneficiary of the 401k is their daughter, the daughter will ultimately receive the account if no changes are made.

How Park Piedmont Can Help in the Estate Planning Process

Some of the most important parts of any estate plan are wills, trusts, and powers of attorney. While Park Piedmont cannot assist with drafting these documents, there are a variety of ways in which we can aid in the estate planning process.

First, we can advise on the optimal way to set up and title accounts to best align with your needs. We can also help with converting individual investment accounts, which are a form of sole ownership, to TOD, Joint, or Trust accounts to avoid probate.

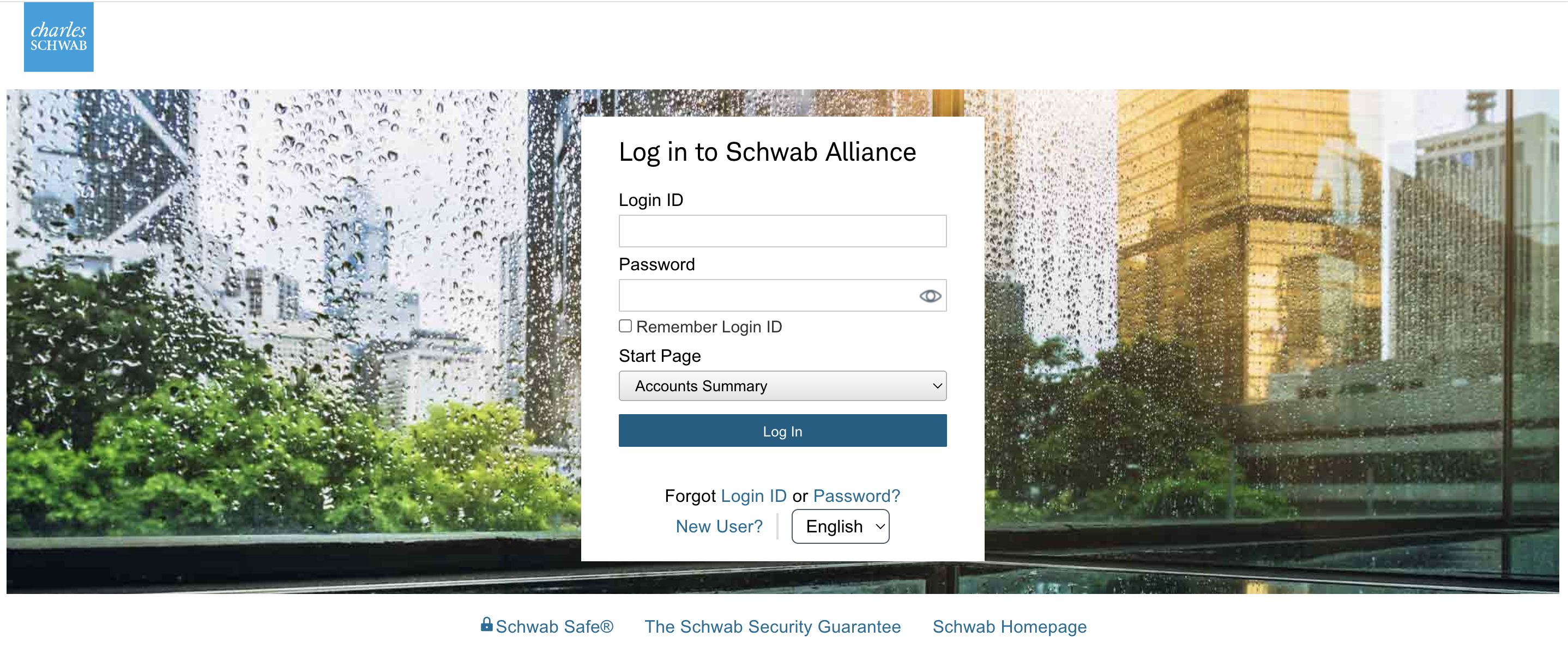

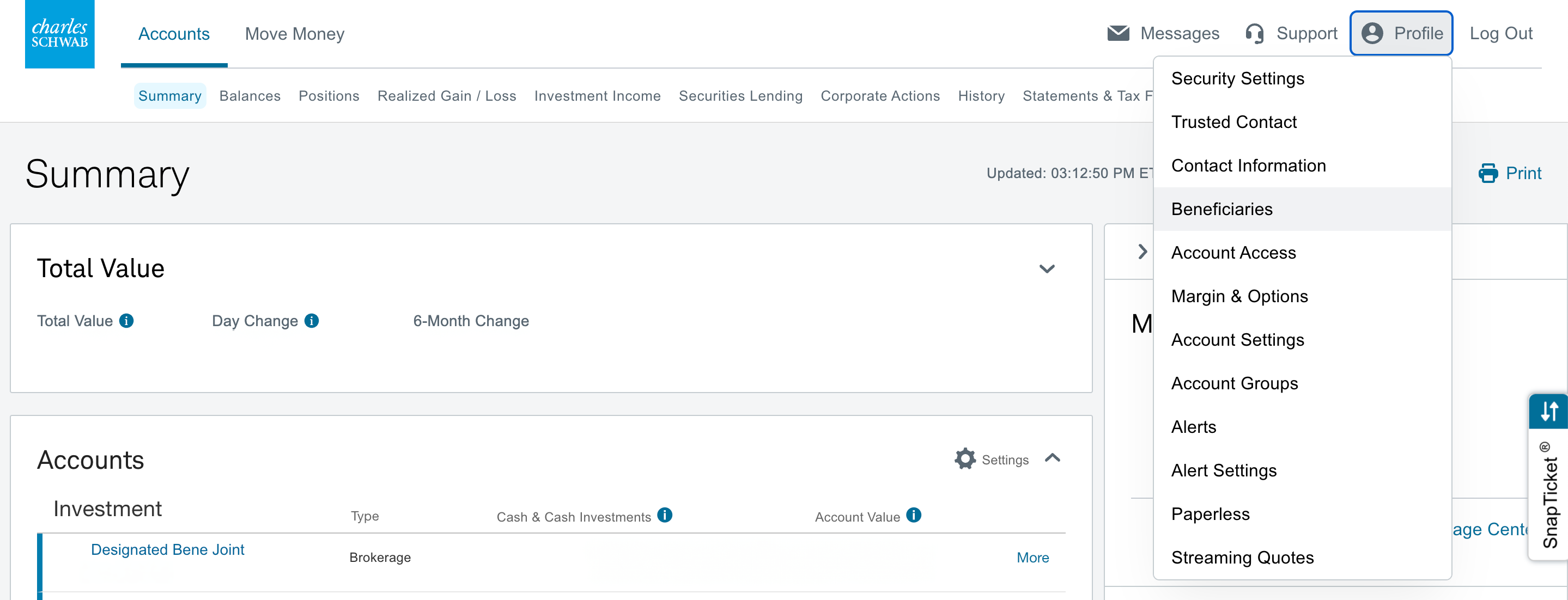

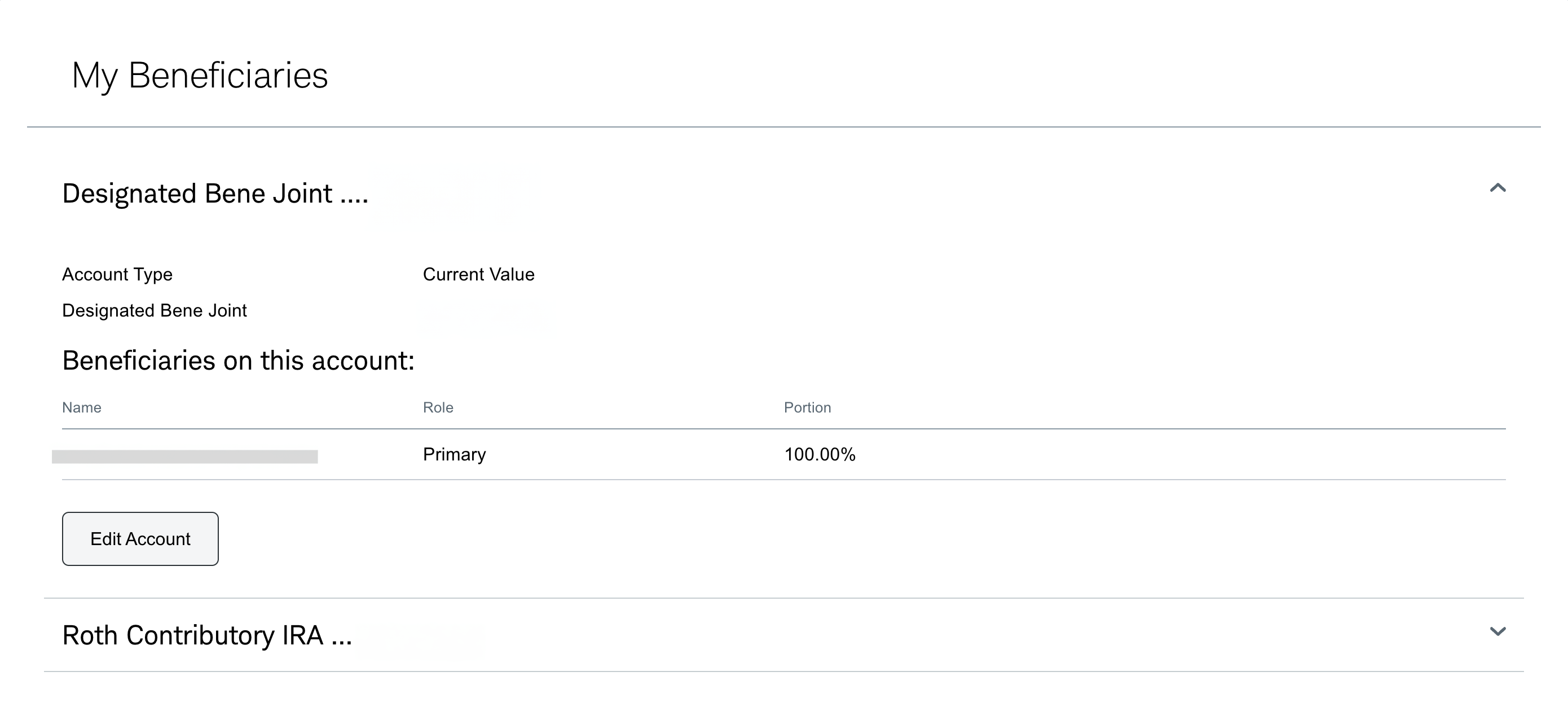

Finally, we can add, remove, or update beneficiary designations on the accounts we manage. Please reach out to your advisor to verify the beneficiary designations on your accounts are up to date and reflect your wishes. Or, see below for instructions on how to add or update a beneficiary in Schwab Alliance on your own.

[Note: Check out our Tax Cuts and Jobs Act update for insights into how federal legislation set to expire at the end of 2025 may impact estate planning and the income tax system more generally.]

How to Add or Update a Beneficiary in Schwab Alliance

“Our approach to investing flows from a single, bedrock principle: the future is unpredictable and uncertain. Indeed – and this is actually quite interesting – even having knowledge of the future doesn’t provide actionable insight as to how markets will behave given that future.”

So begins our book, Thinking About Investing: Two Decades of Reflective Commentary on Markets and Money.

Each of the book’s ten chapters represents a core investing principle and features a selection of commentary previously shared through our newsletters since the firm’s founding in October 2003.

The opening selection, written in February 2014 by our late cofounder Victor Levinson, supports our bedrock principle. It is as relevant today as it was then:

• • •

The financial media and most professional investment organizations (advisory firms, brokerage firms, mutual funds) spend a great deal of time and effort providing their views of the future, either related to the general economy, the prospects of specific companies, or the movement of market prices.

And many in the investing public want to believe that someone out there knows what is going to happen. Unfortunately, the markets prove over and over that they cannot be predicted in advance, frustrating professionals and amateurs alike.

Over the years we have discussed this viewpoint many times. But most people remain skeptical, continually asking the same basic question, even though the terminology of the questions is ever-changing.

The question they want answered is: What is the market likely to do over the next “fill-in-the-blank” time period?

And when we answer that we simply do not know – and what is more, that no one knows, and to think that anyone knows can be a real disservice to a person’s financial well-being – there is always lingering doubt on the part of the questioner.

However, we think we are only stating the obvious: that no one can predict the future and that future stock prices, bond prices, interest rates, or economic growth rates are all subject to unpredictable future events.

Financial media and financial organizations wanting you to believe that someone knows the future is of course in their interest, so you will buy their reports, or research, or investment products, but unfortunately these efforts are all, in our view, an exercise in futility.

Since we recently expressed gratitude for the generations of advisors and clients at Park Piedmont, we wanted to highlight one family we’ve been working with for decades.

Bernard (Buddy) Rosenbaum is an Industrial/Organizational Psychologist with a doctorate degree from Columbia University. Buddy began working with Park Piedmont co-founder Vic Levinson before Park Piedmont existed. Though the firm wasn’t founded until 2003, Vic was already advising clients with the same investment philosophy that guides Park Piedmont today.

Buddy Rosenbaum and Vic shared a love for Central Park. “That was our office,” Buddy said recently. “We had a bench in Central Park, and that’s where we would have our meetings.”

Over the years, three generations of Rosenbaums – Buddy and his wife Linda, their three adult children and partners, and now several of their grandchildren – have worked with three generations of Levinsons, making the relationship a special one.

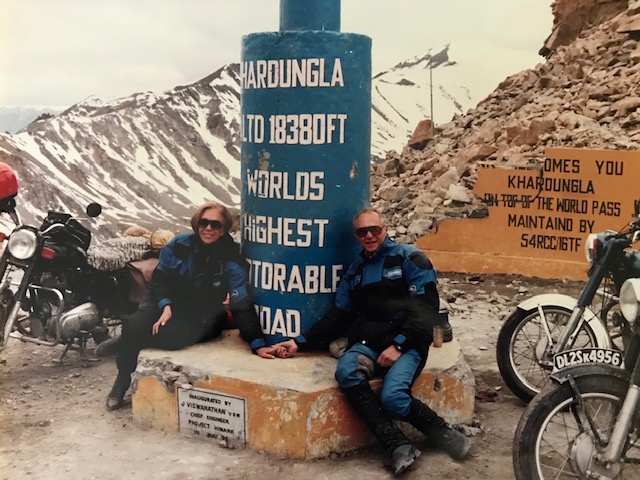

We caught up with Buddy Rosenbaum the week of his 87th birthday, and he charmed us with stories of his life with money – and his remarkable life on a motorcycle.

What is your earliest money-related memory?

My earliest memory of money is getting a wooden vegetable box from Mr. Horowitz, the local vegetable store man, and taking the vegetable box and 30 or 40 old comic books to the local underground subway station.

I set up my stand – the wooden vegetable box – right at the top of the steps where people were coming out of the subway. For new, the comic books would have cost 10 cents, but I was very entrepreneurial. I must have been about nine or 10, and I was selling them for four and five cents.

The following week, another fellow from the neighborhood – Brucey was his name – came with comic books that were in somewhat better shape than mine. He was selling them for the retail price of 10 cents, and he couldn’t understand why mine just flew off the vegetable box and his didn’t. So that’s my earliest money memory.

What is one purchase you’ve made that felt especially weighty – or filled with possibility?

I had a consulting firm, and I brought some partners into the firm. I made a decision at that point that I would treat myself to a luxury item that I had wanted all my life, and I bought a motorcycle.

I was 41 or 42, and it was one of the greatest decisions because my wife accompanied me on many, many tours. We were adventure travelers from that point on. We toured a good part of the world – most of Europe, Nepal, parts of India, Patagonia, South America – all on motorcycle.

A motorcycle opens the world to you, and it opens people to you too. You’re very approachable on a motorcycle. In a car, you’re protected – you have to roll down a window if you want to talk to somebody. But you’re very accessible on a motorcycle, so you get to meet people that normally you would never interact with. And that’s true in the most remote places as well.

Wow, that’s amazing. Was your wife immediately on board?

I wouldn’t say she was immediately on board, but she wasn’t negative about it. We did some local touring – we went up to Nova Scotia, and that was a big distance at the time.

But then I saw an ad – the one and only motorcycle ad probably ever run in New Yorker Magazine. This tiny ad said, “Ride your motorcycle in the Alps.” And I said, “Oh my god. Can you imagine that, Linda? Riding a motorcycle in the Alps?”

So we signed up, and it was a European touring company located in Austria. When we arrived at the airport, Werna was waiting for us, and I said, “Werna, how did the other tours go so far?” He said, “We’ve had no problems.” Great! I later found out we were the first ones he ever did this with.

Linda was involved on a part-time basis at a local travel agency. And it was her idea to represent this motorcycle company in America, so motorcycle touring became her specialty at the travel agency. They’re the world’s biggest in motorcycle touring now – it’s a company called Edelweiss Bike Travel – and she helped to establish them in America. So that was her involvement. She knew more about motorcycles than I did at the end.

Linda and Buddy Rosenbaum at Khardung La Pass, one of the world’s highest motorable roads, located in Ladakh, India.

Do you have a favorite destination?

Nothing is better than the Alps for riding. We’ve done that many times. But if you expand it to not just the riding challenge but the touring interest, everywhere. We’ve done most of Europe. The longest was with a friend for six weeks. We rented motorcycles and started in Heidelberg, then went up to the northerly most point in Europe, Nordkapp in Norway. We came down through Finland and into Russia, then back through Lithuania and Estonia and so on. But I can’t pick a favorite. We did Patagonia, Nepal, Bhutan…

What do you wish you could tell your 20-year-old self about life with money?

At 20, I knew what I wanted to do with money. It wasn’t the pursuit of money unto itself, but I wanted the freedom that some degree of financial security would provide. The freedom to make choices – not necessarily the choices for survival but for the choices of enrichment.

And I did have a foundational need for security. I got married at a very early age, and we had kids at a very early age. So economic security was very important to me. And all this avocational activity – like the motorcycling – came at around age 40. But up to that point, I was kind of obsessively involved with building my consulting firm. And by the nature of that activity, there was a lot of travel. I was away two to three nights a week for most of that time. And that’s when I brought partners into the business.

Was there ever a decision you made, or a step you took, that made your life with money less stressful?

I think making the decision to bring my partners into the business, which I made pretty early on – somewhere around age 40. It sounds odd: the business wouldn’t necessarily grow in exactly the way I wanted it to, though close enough, but I would also have, early on, some degree of economic security to diversify some of the things I would be doing. I was itching to do some discretionary travel.

What is the best gift you’ve ever received?

Well, I’m thinking about where I am right now [in East Hampton] … A few years ago, my oldest son bought me the world’s greatest beach chair. It had a little umbrella, it had a place for your drink, it had all kinds of different seating positions. Great beach chair! It made going to the beach so much more comfortable. I could strap it onto my back and bicycle to the beach. Terrific gift!

Is there anything else you want to share about life with money?

Meeting and working with Vic allowed me to focus far more on the satisfying and gratifying things in life, rather than checking the New York Times finance section every day. Vic’s investment philosophy squelched the question, “Is the market up or down today?” It was so gratifying, and even liberating, to not have to think about that. So in that sense, there was a liberating dimension of life that came from working with Vic, and now Park Piedmont.

A PBS documentary featured Buddy Rosenbaum, at age 72, and a friend as they rode motorcycles from San Francisco to New York City via the Lincoln Highway. A party welcomed the two when they arrived in Times Square.

As Park Piedmont moves into its third decade serving our clients, I wanted to share a few personal reflections on our family firm.

First, we’ve been very fortunate to see the firm grow significantly over the years. Initially, in 2003, Vic and I worked just with Lynette, who many of you will remember as our longtime, beloved Client Service guru. Tom joined in 2014 and has been a key firm leader while also bringing an important focus on life planning to the more technical work of money management. The advisory team expanded further with the addition of Samantha in 2021 and my son Nate in 2022.

To complement this additional capacity on the advisory side, we’ve added staff to provide outstanding client service. Ana now leads the Client Service team, which includes Leslie, Kathryn, and, most recently, Heather. We have Amanda focusing on operations, and Corenna on education and marketing. We also continue to work closely with our three CPAs/advisors, Richard, George, and Stu.

Even as we’ve grown, we’ve worked hard to retain the feeling and values of a small family firm. The entire team is committed to providing thoughtful, unbiased, comprehensive financial advice to all of you.

Second, we continually strive to honor Vic’s legacy. He was a great advisor and teacher, and demonstrated a total commitment to helping clients achieve their goals throughout their various stages of life and wealth. He set an example for us, both professionally and of course personally, and we know he would be thrilled to see that a third generation of our family is now part of the Park Piedmont team.

Speaking of Nate, we were overjoyed to celebrate his wedding last month! We spent a great week with family and friends in Minneapolis, where his wife Nuria grew up, culminating in a really fun ceremony and party. Nate and Nuria have been together since sophomore year of college, and are moving to Cincinnati, where Nuria has an internship as part of her clinical psychology training.

Finally, as Park Piedmont started and has continued as a family firm, we also celebrate the opportunity to provide advice and peace of mind to multiple generations of many client families. We spend a lot of time making sure that the transitions among generations of Park Piedmont advisors and clients go as smoothly as possible and continue to serve your needs. We are especially excited, for example, to see Sam and Nate beginning to advise third-generation clients.

This family continuity was a primary goal of ours when we founded the firm, and we’re honored that so many of you, of all generations, continue to place your trust in us.

This website or its third-party tools use cookies, which are necessary for its functioning and required to achieve the purposes illustrated in our privacy notice. If you want to learn more or withdraw your consent to all or some of the cookies, please refer to our privacy notice. You accept the use of cookies by closing or dismissing this banner, by clicking a link or button, or by continuing to browse otherwise. ACCEPT

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are as essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Get our new book Thinking About Investing – our guiding principles on how to invest.