OBSERVATIONS ON NOVEMBER 2018 STOCK and BOND MARKETS

Two front page headlines from the NY Times, nine days apart, tell a good deal about November volatility, both up and down, for the US stock markets: On November 19th (NYT, 11/19/18, page A1), “Tech Stocks Dive as Wall Street Loses Gains for Month,” and then November 28th (NYT, 11/28/18, page A1), “Markets Soar on Two Words From Fed Chairman.” By the time November ended, the three major US indexes all showed modest month and YTD gains (see page 1).

NOTE: The closing value of the S&P 500 on November 19th (as reported in the 11/19/18 article), was 2,691, and the closing value on November 28th (as reported in 11/28/18 article), was 2,744, a 2% difference. The range of high and low for the month was 2,632 (November 23rd close), to 2,814 (November 7th close), a 7% difference measured from the low. By way of comparison, 2018 has had four other months of similar or higher volatility.

We will spare you the repetition of the media’s discussions of the day to day reasons for all this volatility, and instead acknowledge that the current financial markets are likely being driven more by current events than by fundamental economics. That said, there is still no reason to change your previously established asset allocations to and away from stocks, even with all this volatility. Long term investors learn to ignore the not uncommon, and noticeable, fluctuations in stock prices.

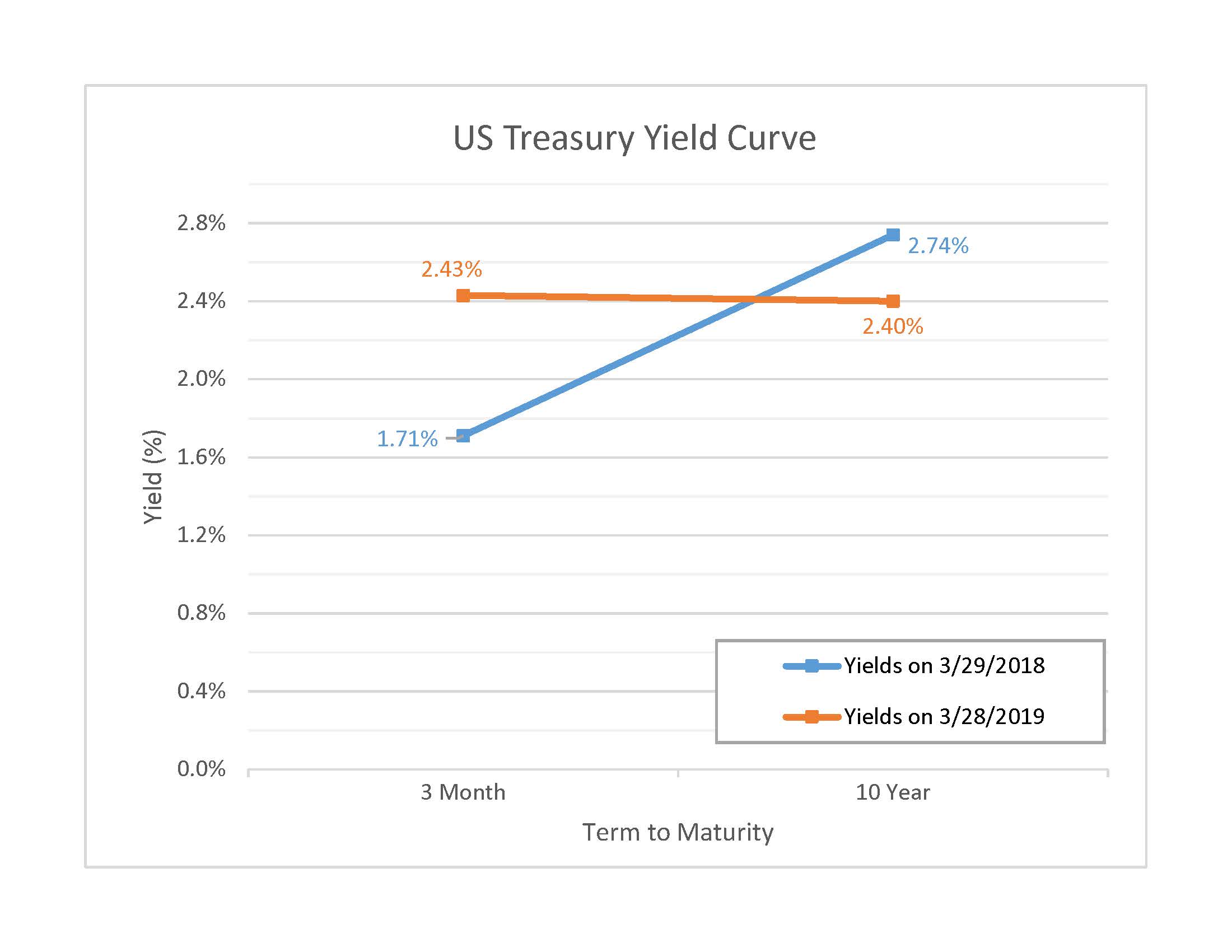

Turning to bond prices, they were modestly higher in November, as interest rates on the ten-year US Treasury declined from 3.16% to 3.0%. This was surprising, because higher interest rates have been presented as one of the main reasons for the recent stock market declines (even though they had been increasing for much of this year, while stock prices moved higher until the end of September). The above mentioned November 28th article provides a rationale for this situation: the Fed may be close to ending its program of increasing interest rates in the future, which presumably benefits stock prices. But, as we always point out, stock prices are impacted by many more factors than just interest rates, whereas bonds are impacted almost most entirely by interest rates.

EARLY DECEMBER UPDATE

When preparing our Monthly Comments, it is our practice to limit the discussion to the month about which we are writing. That said, we want you to know we are keenly aware of the early December market volatility, and stand ready to write additional one page Special Comments as warranted. We note that as of the close of December 6th, after an extremely volatile day ending with a small change, the S&P 500 index is still slightly above its year end 2017 level, and its recent February and October 2018 lows.

PPA BOOK CORNER: FACTFULNESS

We recently read a book we found very interesting, with some relevance to the financial issues we work on with you. It’s called Factfulness, by Swedish physician Hans Rosling, and we encourage you to take a look if you have some time.

In the face of much bad news in the world today (financial and otherwise), Rosling seeks to provide fact-based information to counter ten “instincts”, or barriers, that he claims prevent people from acknowledging many slow, steady improvements. He uses UN data to show, for example, that extreme poverty is declining and life expectancy is increasing in almost all countries. And he offers useful advice to help us understand that while certain situations continue to be bad, they are getting better.

Chief among these barriers is the “gap instinct”, or the propensity to see the world in binary terms – us vs. them, “the west and the rest”, developed vs developing countries—when the reality is much more complicated. Rosling presents a fascinating graphic on the inside front cover of the book that plots incomes and lifespan (his surrogates for overall wealth and health) for all 195 countries across the globe. Instead of dividing the world in two, he frames almost every discussion in the book around an analysis of four basic income levels, and focuses on how almost all countries have moved up and to the right on this chart (i.e., to more wealth and better health) over the past two centuries. (See YouTube also for a fascinating video called 200 countries, 200 years, 4 minutes, which illustrates the fluidity of this phenomenon.

The next major barrier is the “negativity instinct”, which involves an often vicious cycle of media reporting bad news – war, violence, scandal—and people thinking that’s the only news out there. Rosling again urges readers to look beyond the scary headlines to data showing improvements in many areas. He presents charts of 16 “bad things decreasing”, including many diseases, hunger, deaths from disasters, and environmental toxins, and 16 “good things increasing”, including girls in school, literacy and immunization rates, “protected” nature and clean water (pages 60-63). Rosling doesn’t want to be seen as a Pollyanna, but neither does he assume the cynical tone of the eternal pessimist. Instead, he considers himself a “possibilist”, acknowledging that while much work needs to be done, much can, and already has been, improved.

The third significant barrier is the “straight lines instinct”, in which people assume that troubling trends will continue at the same rate, instead of leveling off or even declining due to changes that reflect broader improvements. Rosling’s main example here is population increases, which have rocketed upward in the past 100 years. But according to UN forecasts, these increases are expected to grow less quickly over the next 100 years, due to declining birth rates that in turn stem from less poverty, better education, and more access to contraception in lower income countries (pages 80-86). More generally, instead of projecting from just two data points, Rosling encourages the search for additional data that might reveal the real long-term trend.

Rosling also addresses a number of relevant financial issues in the context of other barriers. Related to the “fear instinct”, he criticizes the media (page 104) for its often short-term thinking and scare tactics, a view PPA shares often in our monthly commentaries. Rosling provides a useful distinction between perceived risk (or fear) and real risk, which he calculates as danger multiplied by exposure (page 123). This is a helpful way to think about balancing risk and return in your portfolios, specifically by raising or lowering your allocation to stocks (i.e., adjusting your exposure to the “dangerous”, or most volatile, part of the markets). In his discussion about the “urgency instinct”, Rosling explains how we tend to focus on present risks (e.g., daily or monthly ups and, especially, downs in the markets) as opposed to future risks, such as not saving enough for retirement (page 228). He also encourages going beyond a single estimate (page 231), and instead testing at least three scenarios when making projections (e.g., expected, better, and worse), which PPA typically does with your retirement illustrations. And in terms of specific thoughts on investing, Rosling discusses the “destiny instinct” in encouraging investors not to dismiss opportunities in poor but growing parts of Africa, Asia, and South America (page 167). This might lead to an additional allocation to “emerging market” or even “frontier market” stock funds for the international stock part of your overall portfolio.

Sadly, Rosling died in 2017 (his son and daughter-in-law finished the book and continue his work). But his writing inspires an infectious enthusiasm for his wide-ranging interests, and we greatly appreciate his concluding plea for humility and curiosity: be humble in the context of a growing, uncertain world, and remain curious about other people, ideas, and possibilities for improvement.